uses debt to a moderate extent")

Warren Buffett once said, “Volatility is far from being synonymous with risk.” So it is obvious that you have to take debt into account when thinking about how risky a particular stock is, because too much debt can ruin a company. We find that Wonder Information Co., Ltd. (SZSE:300168) has debt on its balance sheet. The real question, however, is whether this debt makes the company a risk.

Why is debt risky?

Generally, debt only becomes a real problem when a company can’t easily pay it back, either by raising capital or through its own cash flow. A key part of capitalism is the process of “creative destruction,” in which failed companies are mercilessly liquidated by their bankers. A more common (but still costly) situation, however, is when a company must dilute shareholders at a cheap share price just to get the debt under control. However, the most common situation is when a company manages its debt reasonably well – and to its own benefit. The first step in looking at a company’s debt levels is to look at its cash and debt together.

Check out our latest analysis for Miracle Information

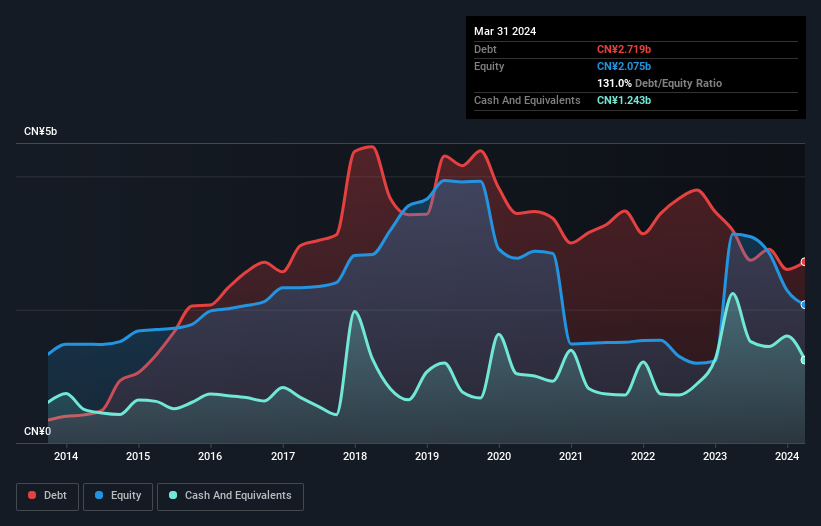

What is Wonders Information’s net debt?

You can click on the chart below to see the historical numbers, but it shows that Wonders Information had CN¥2.72 billion in debt as of March 2024, up from CN¥3.19 billion a year earlier. However, this compares to CN¥1.24 billion in cash, resulting in net debt of about CN¥1.48 billion.

How healthy is Wonders Information’s balance sheet?

According to the most recent balance sheet data, Wonders Information had liabilities of CNY3.80 billion due within one year and liabilities of CNY799.1 million due thereafter, compared with cash of CNY1.24 billion and receivables of CNY1.31 billion due within 12 months. So liabilities exceed the sum of cash and (short-term) receivables by CNY2.05 billion.

Wonders Information has a market capitalization of CN¥7.09b, so it could very likely raise money to improve its balance sheet should the need arise. But it’s clear that we should look closely at whether the company can manage its debt without dilution. There’s no doubt that we learn the most about debt from the balance sheet. But it’s future earnings, more than anything, that will determine whether Wonders Information can maintain a healthy balance sheet going forward. So if you’re focused on the future, this is where you might want to look. free Report with analysts’ profit forecasts.

On a 12-month basis, Wonders Information posted losses at EBIT level and its revenue fell to 2.1 billion Chinese yen, a decline of 30%. Frankly, this does not bode well.

Reservation by the buyer

Not only have Wonders Information’s revenues declined over the past twelve months, the company has also posted negative earnings before interest and tax (EBIT). In fact, it lost a sizeable CNY980m at the EBIT level. When we look at this and recall the liabilities on the balance sheet relative to its cash holdings, it seems unwise to us that the company has debt. Frankly, we think the balance sheet is far from balanced, although it could be improved over time. However, it doesn’t help that it burned through CNY363m in cash last year. So suffice it to say that we think the stock is very risky. When analyzing debt levels, the balance sheet is the obvious place to start. But ultimately, any company can contain risks that exist outside the balance sheet. Case in point: we found 2 Warning Signs for Miracle Information You should be aware of these, and one of them is a little uncomfortable.

If you are interested in investing in companies that can grow profits without the burden of debt, check this out free List of growing companies that have net cash on their balance sheet.

Valuation is complex, but we are here to simplify it.

Discover whether Wonders Information might be undervalued or overvalued with our detailed analysis, with Fair value estimates, potential risks, dividends, insider trading and the company’s financial condition.

Access to free analyses

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.