")

Kittisak Kaewchalun /iStock via Getty Images

introduction

Note: Investors should consider this article an update to my previous article on Avance Gas.

Avance Gas Holding (OTCPK:AVACF) announced in August the sale of its entire VLGC fleet 15. The competitor BW LPG (BWLP) will buy AVACF’s ten VLGCs for a total of $1.05 billion, in addition to the two vessels currently under sale-and-leaseback (novation) agreements. AVACF cited size and efficiency as reasons for divesting its relatively small VLGC fleet to larger competitor BW LPG, which owned and operated 43 vessels prior to the transaction.

Another factor was probably the realisation of the enormous profit from his fleet compared to the original purchase price. His most prominent owner, the John Fredriksen group of investment companies, had in the wake of the booming VLGC market in the last few years.

The transaction will be settled for $585 million in cash, a 12.77% interest in BW LPG ($17.25/share) and a novation of the SLB agreements for $132 million. The interest in BW LPG is valued at $333 million. For comparison, BW LPG closed at $16.16 on Wednesday, August 14.

The market reacted by pushing the share price down to NOK 154.40 after a brief run above NOK 180. Ultimately, AVACF ended the day down about 11% on heavy volume. In the early hours of August 16, the share was trading in the range of NOK 156-160.

What does this deal mean for Avance Gas? Let’s take a closer look.

A brief overview of Avance Gas Holding

AVACF is a Bermuda-based VLGC tonnage operator listed on the Oslo Stock Exchange. It is one of shipping magnate John Fredriksen’s portfolio companies, in which he is a majority owner through one of his family’s investment vehicles. Until a few days ago, the company owned and operated a fleet of 12 VLGCs with an average age of just six years. In addition, it had ordered four MGCs after announcing in mid-2023 that it saw a bright future for medium-sized gas carriers and the future of the ammonia trade.

As mentioned in my previous article linked above, the company’s main focus was to return money to its shareholders through a “as high as possible and as predictable as possible” dividend policy. As is often seen in Mr. Fredriksen’s portfolio, AVACF has not been afraid to leverage its business and has maintained a relatively higher level of debt than its peers. Nevertheless, the company has been very successful.

In addition to the market and geopolitical risks that apply to gas transporters, AVACF faces additional risk due to its listing in Oslo in NOK. The NOK is the least liquid of the G10 currencies and is at a 15-year low compared to its trading partners. The problems caused by this volatility were one of the main reasons for competitor BW LPG to list its shares on the NYSE. However, AVACF remained only on the Oslo Stock Exchange.

Avance Gas Holding Ltd. is now truly a holding company

Following the transaction, Avance Gas

- no fleet on the water, but newbuilding contracts for four MGCs (40,000 cbm), delivery planned from Q4 2025

- The company holds a 12.77% stake in its competitor BW LPG, making it the second largest shareholder.

- nearly $500 million in cash (the NewsWeb article above reports net proceeds of $217 million, in addition to the $257 million cash balance reported in May)

In an interview with Norwegian daily Finansavisen, CEO Oystein Kalleklev said the company was considering transferring its shares in BW LPG to its shareholders and additionally paying an irregular dividend from the sale.

The sale marks another milestone in AVACF’s transition to the mid-range segment and ammonia trading. In June 2023, the company announced an order for two MGCs and declared an option for two more shortly thereafter. CEO Kalleklev said: “Given the expected high growth of the ammonia trade, this makes the vessels a very attractive addition to our fleet.”

The agreed price was $61.5 million per vessel. According to the CEO of AVACF in the interview mentioned above, the company currently has an unrealized profit on these newbuilding contracts, as each vessel is currently worth about $72 million.

Over the past year, the company has announced the sale of its VLGCs on several occasions:

- Iris Glory built in 2008 (July 2023)

- Two new builds scheduled for delivery in 2024 (December 2023)

- Venus Glory built in 2008 (March 2024)

- Another new building (March 2024)

- Another new building (May 2024)

In summary, AVACF has exited the VLGC segment – at least as a direct player – and is now positioned for an expected increase in ammonia trade. The ordered MGCs are designed to transport LPG and NH3 (ammonia).

Will this bet pay off?

Concluding remarks

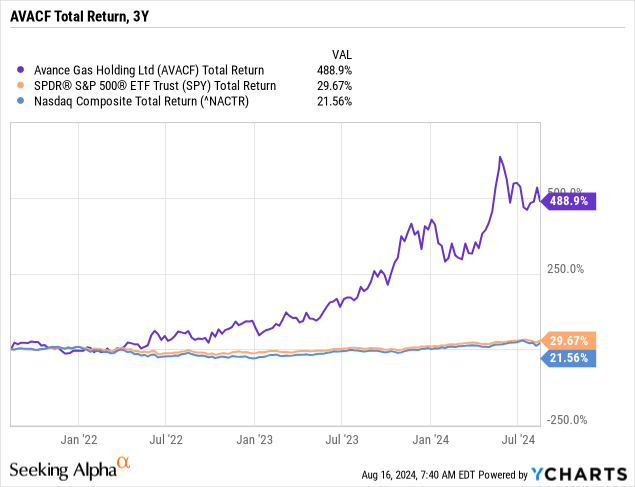

For existing investors, the last few years have been exceptional. If you had bought and held AVACF near its low point (from 2018 to 2021, the price moved roughly sideways), you would have had a fantastic ride:

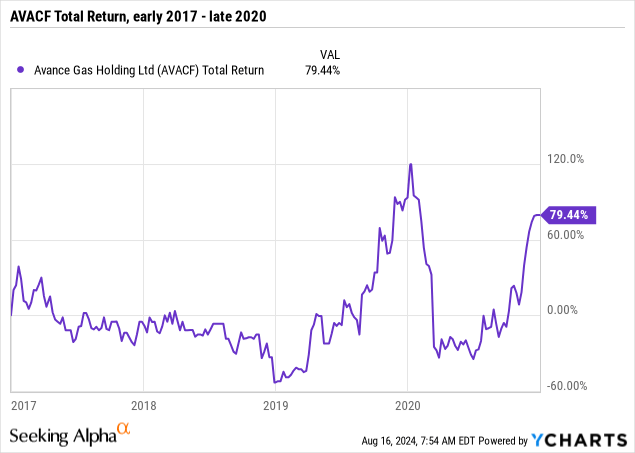

But unfortunately, investors don’t make money on past earnings, but on future ones. You could base your decision on John Fredriksen’s track record of creating shareholder value over many years, but even then you would risk having your patience tested. Consider AVACF’s total return between the beginning of 2017 and the end of 2020:

For most of the period, you would probably get better returns elsewhere.

AVACF’s future ability to generate attractive returns for its shareholders will depend on the prospects of the maritime LPG trade – through its small fleet and its indirect involvement through its stake in BW LPG – and the growth in the maritime ammonia trade. I believe that AVACF is likely to divest its stake in BW LPG (distribute shares to its shareholders) and therefore the growth in the maritime ammonia trade will become relatively more important.

Hellenic previously reported that the ammonia trade is “on the verge of exploding,” citing a forecast that ammonia demand will increase massively in the coming years. While demand is expected to grow in East Asia and Europe, production will take place in the Middle East and Australia, resulting in ton-miles. Mordor Intelligence expects only a 1.89% compound annual growth rate through 2029.

Ammonia is very dangerous; some of its promises are related to “green ammonia”. Much like other promising substances such as “green hydrogen” and “green methanol”, “green” ammonia will compete for the same limited available amount of so-called “green” electricity. Building supply chains and power grids to support new forms of electricity generation takes time and is costly. This only underlines the challenge for ship owners: which fuel(s) will be the future winners?

The “safe” answer seems to be “a mix.”

Maersk recently backed away from its LNG-free pledge and has ordered up to 60 LNG-powered vessels. Maersk CEO said:

(..) the industry will be faced with a mix of fuels such as methanol and LNG for a longer period than expected, with great uncertainty about their availability and costs.

Chevron’s new project in the Gulf of Mexico is developing previously untapped oil reserves and could extend drilling opportunities in the Gulf for years. This means there will be more oil available to the market, and this is just one project of many.

Maersk and Chevron are just two examples of the complexity of the ongoing effort to move away from fossil fuels.

In summary, the seaborne ammonia trade is likely to grow, but the complexity of changing supply chains and competition from other new and existing fuels will complicate things. Given the track record of AVACF’s management and majority owner, I am confident they will be able to generate returns for shareholders in the future. However, I am concerned that AVACF has only just reached its potential in the short term, meaning any investor considering entering the stock should be patient.

Investors would be remiss to consider the current valuation. The stock closed at NOK 150.40 on Friday, August 16, giving the company’s 77.4 million shares a value of NOK 11.6 billion. Using the last available NOK/USD rate from the central bank (1 USD = 10.75 NOK), AVACF is valued at USD 1.08 billion. AVACF’s remaining assets, as mentioned above, include about USD 500 million in cash and a USD 333 million stake in BW LPG, totaling about USD 800-850 million. A fair value based on this would be USD 10.34-10.99, or about NOK 111-118. In other words, AVACF appears to be trading at a premium. However, as I noted in my previous article, this stock has historically traded at a premium to comparable stocks. I would call this the “Fredriksen effect,” the tendency of a stock to trade at a premium to its peers because it has a visible, active and, to be fair, successful majority owner. Going back to my previous article, the basic thesis remains the same: this company has an excellent management record and is likely to continue to be successful, but it is relatively expensive – which may deter some investors.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these securities.